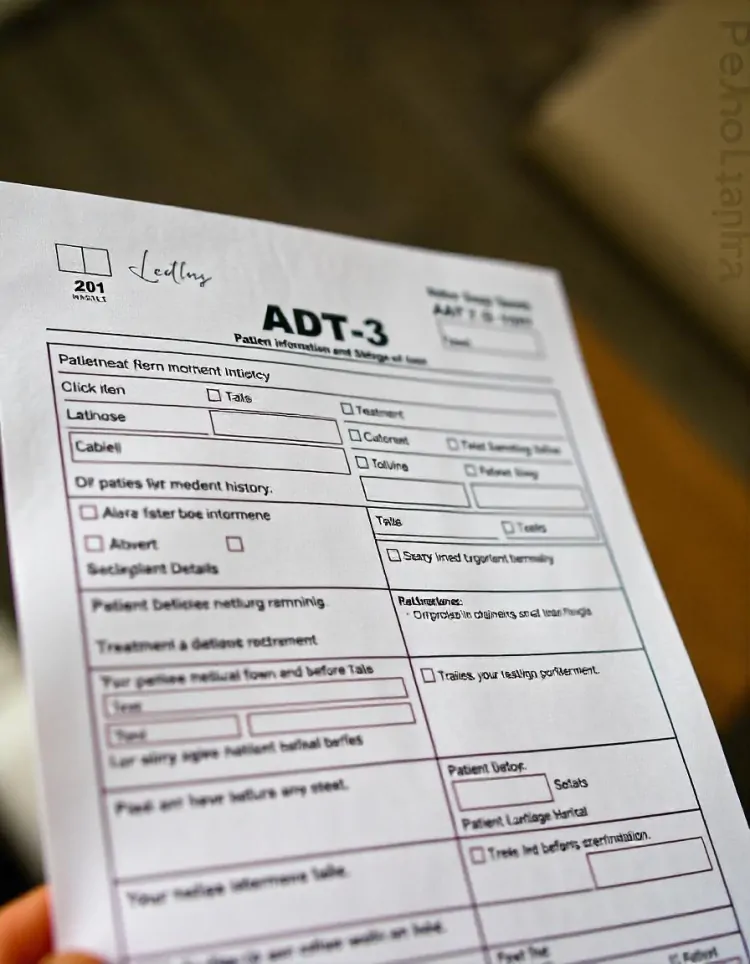

What Is the ADT-3 Form and What Is Its Purpose in Compliance?

The ADT-3 form is a crucial document mandated under the Companies Act, 2013. It is filed by auditors to notify the Registrar of Companies (RoC) about their resignation from the position of auditor in a company.

Compliance with corporate laws is crucial for businesses to maintain transparency and accountability. Among the various forms required under the Companies Act, 2013, the ADT-3 form is significant, especially concerning the resignation or removal of an auditor. In this blog, we’ll explore what the ADT-3 form is, its purpose, and why it is essential for corporate compliance.

Understanding the ADT-3 Form

The ADT-3 form is a crucial document mandated under the Companies Act, 2013. It is filed by auditors to notify the Registrar of Companies (RoC) about their resignation from the position of auditor in a company. This form ensures that the departure of an auditor is documented, providing a transparent mechanism for the management of statutory audits.

Why Is the ADT-3 Form Important?

-

Maintaining Transparency

The ADT-3 form ensures that the reasons behind an auditor’s resignation are recorded with the RoC. This promotes transparency between the company, its stakeholders, and regulatory authorities.

-

Facilitating Compliance

Filing the ADT-3 form is a legal obligation under Section 140(2) of the Companies Act, 2013. Non-compliance may lead to penalties and other legal consequences for the auditor.

-

Protecting Auditor’s Interest

By filing the ADT-3 form, auditors safeguard themselves from any future liabilities or disputes arising from their resignation. It serves as a formal notice to the government, clearing the auditor’s responsibilities.

When Should the ADT-3 Form Be Filed?

Auditors are required to file the ADT-3 form within 30 days of their resignation. Timely filing is crucial to avoid penalties under the Companies Act, 2013.

Step-by-Step Process to File the ADT-3 Form

Step 1: Obtain the Form

The ADT-3 form can be downloaded from the Ministry of Corporate Affairs (MCA) website.

Step 2: Fill in the Details

Provide the following information in the form:

-

Name and address of the auditor.

-

Name and CIN (Corporate Identification Number) of the company.

-

Date and reason for resignation.

Step 3: Attach Supporting Documents

Attach a detailed resignation letter addressed to the company and other relevant documents explaining the reason for resignation.

Step 4: Submit the Form

The completed form must be filed online on the MCA portal, along with the prescribed filing fee.

Purpose of the ADT-3 Form in Compliance

The primary ADT-3 form purpose is to ensure compliance and accountability in the auditing process. Below are its main purposes:

1. Regulatory Oversight

The form enables the RoC to monitor changes in a company’s auditors and investigate irregularities, if any.

2. Clarity for Stakeholders

Stakeholders, including shareholders and investors, are informed of the auditor’s resignation and its reasons, maintaining trust and confidence.

3. Legal Safeguards

Filing the ADT-3 form legally frees the auditor from any further obligations or liabilities regarding the company.

Consequences of Not Filing the ADT-3 Form

Failing to file the ADT-3 form can lead to severe repercussions, such as:

-

Financial Penalties: Auditors may face fines for non-compliance under the Companies Act, 2013.

-

Reputational Damage: Non-compliance may tarnish the professional image of the auditor.

-

Legal Actions: The RoC can take legal action for not adhering to mandatory compliance norms.

Common Scenarios Where the ADT-3 Form Is Filed

1. Voluntary Resignation by an Auditor

Auditors may resign for personal reasons or professional conflicts, requiring the ADT-3 form filing.

2. Removal by the Company

If a company removes an auditor before their term ends, the auditor may file the ADT-3 form to record the reason and safeguard their interests.

3. End of Audit Term

Although not mandatory, some auditors choose to file the ADT-3 form after completing their terms for clarity and documentation.

Key Points to Remember About the ADT-3 Form

-

Filing the ADT-3 form is mandatory under Section 140(2) of the Companies Act, 2013.

-

The form must be filed within 30 days of resignation.

-

Supporting documents, including the resignation letter, must be attached.

-

It ensures compliance, transparency, and legal safeguards for auditors.

FAQs on the ADT-3 Form

1. Is the ADT-3 form applicable to all companies?

Yes, the ADT-3 form is applicable to all companies governed by the Companies Act, 2013.

2. What happens if an auditor doesn’t file the ADT-3 form?

Non-filing can lead to penalties and legal consequences under the Companies Act, 2013.

3. Can the ADT-3 form be filed offline?

No, the form must be filed online through the MCA portal.

4. Who is responsible for filing the ADT-3 form?

The resigning auditor is responsible for filing the ADT-3 form.

Conclusion

The ADT-3 form purpose is to uphold transparency, compliance, and accountability in corporate audits. By filing this form, auditors ensure their resignation is documented and legally binding. It protects their interests while fulfilling regulatory requirements. Whether you’re an auditor or a company, understanding the significance of the ADT-3 form is essential for smooth corporate.

What's Your Reaction?